2017 Predictions

There is something special about the beginning of a new year, slates are wiped, figures are reset, and suddenly, we are working toward new goals, developing new features, and designing new methods for improving productivity, reducing spend, and staying happy. The new year is a good opportunity to look forward, both from a business and a personal perspective, to pre-empt the shifts and transformations on the horizon, to be able to manage change effectively.

So, here are my top three predictions on the factors affecting software spend in 2017, what challenges they present to enterprises, and what impact they may have on your business, your CIO, IT managers, and SAM experts as you work together to optimize IT spend.

#1. Continued adoption of IaaS/SaaS widens the disruption gap

We have been talking about cloud adoption for over a decade, waiting for cloud to go mass market. I believe that 2017 will witness a significant upswing in the uptake of cloud services, a trend that I see continuing until 2020.

Since much of this increase is being funded by business units as opposed to traditional IT department spend, it will drive a related increase in the “disruption gap,” a term Snow developed to describe the delta between what the IT department knows about application usage and cost in the IT estate and what is actually happening.

This year, cloud will pass the critical point of maturity. Innovators and early adopters have proven the underlying technologies, vendors have undergone sufficient iterations to appeal to the mainstream, and the market is now ripe for the early majority to make the shift. Vendors like Amazon, Microsoft, Salesforce.com and Adobe have proven the value of anything-as-a-service – IaaS, PaaS, SaaS – some with record financial results. Paving the way for other vendors and building market uptake.

Adobe achieved record annual revenue of USD 5.85 billion in fiscal year 2016, representing 22 percent year-over-year growth.[i]

In its third quarter release, Salesforce announced an exceptional quarter, with year-over-year revenue growth of 25 percent in dollars and 27 percent in constant currency.[ii]

IAAS

While the benefits of IaaS are clear, there is a price to pay. The cost of IaaS can quickly spiral out of control as it is easy to forget about virtualized services, servers can be left running, feedback loops can cause repetitive downloading, and expensive software can be left idling on forgotten machines.

In 2017, I believe that enterprises will adopt a cloud-first strategy for primary enterprise infrastructure, with only niche industries choosing on-premise as the preferred solution. And I believe the Software Asset Management industry will be critical to providing the insight and control necessary to manage spend.

SAAS

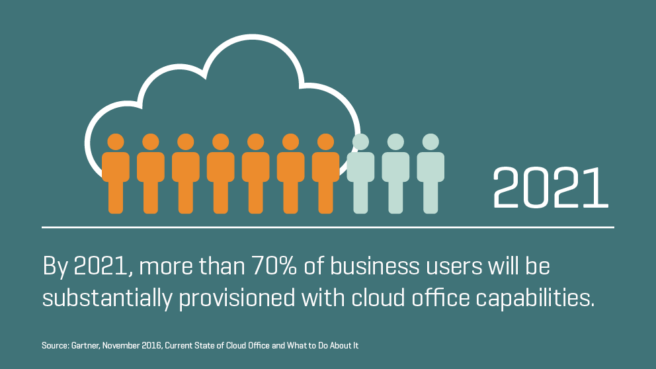

This market is now at a tipping point and uptake will continue to accelerate throughout 2017, driven largely by business unit technology spending that is outside the control and sometimes even knowledge of the IT department. The early majority will start to make the move this year bringing adoption over 50 percent within the next few years. Many organizations have yet to adopt, so there is time to take advantage of the incentives vendors will continue to offer to move customers over to their cloud SaaS solutions. From a compliance perspective, Microsoft, for example, has so far been lenient with customers that are licensed for Office 365 but who continue to use older versions. As mainstream adoption takes place, we can expect that to change and for Microsoft to clamp down on unlicensed use of legacy Office products. I think other vendors are equally likely to ignore legacy usage during the transition period.

All in for the cloud

Whatever cloud office system, SaaS solution, or IaaS you deploy within your organization, optimizing spend depends on visibility to close the growing disruption gap.

Tips for establishing visibility include:

- Establish a holistic view of all installations, not just those resulting from IT department spend

- Don’t rely on individual administrative consoles provided by each SaaS vendor

- Ensure your software asset management program supports visibility into IaaS/SaaS usage

Only with intelligent and consolidated data on IaaS/SaaS installations can spend be optimized.

#2. Merging worlds and increasing abstraction

As technologies mature and global digital transformation deepens, the level of software abstraction and consolidation within IT will rise. New technologies leverage existing assets and at the same time promote cross-platform, cross-vendor, collaboration.

In 2017, I see vendor connectivity accelerating at the same time as we gain deeper abstraction through this connectivity. We can expect deeper system co-operation, in which business and cost insight delivered by one discipline can be leveraged by others. We can expect to move closer to a single pane of glass.

The IT journey

What has happened, on the IT journey from mainframe to cloud is ever-increasing abstraction of details, and ever-increasing system inter-connectivity, which has in turn enabled business users to make decisions on a higher level and with enriched data. IT consolidation has led to a degree of connectivity among disciplines and from a Software Asset Management perspective, our closest cousins include workflow automation (ITOM), services (ITSM) and cost control (ITFM).

Specifically, the consolidation of these disciplines brings together four core business functions – compliance, automation, services, and cost control – enabling organizations to manage risk.

System convergence is not new, software connectors have been around in one form or another for decades, but as cloud adoption accelerates they have achieved an elevated significance. What was once a technical enabler, is today a staple of software development, facilitating the creation of platform and vendor independent business workflows.

Perhaps the greatest benefit of consolidation is the avoidance of vendor lock-in. But at the ground level it reduces, and will eventually remove the need for manually connecting systems. Workflows can be built across multiple systems, from multiple vendors, across business units and corporate functions.

System consolidation breaks down silos. By leveraging data and integrating tools, the walls and barriers that exist between business units, group functions, vendors, and technologies will diminish. And finally, consolidation enables decision-making with an enriched data set and cost transparency.

#3 Tech-savvy demanding users.

In 2017, I envisage enterprises focusing on user satisfaction, not just in terms of providing employees with the tools that they need to be productive, but to embed flexibility in the way services and tools are delivered. Empowering business units to take IT decisions will be critical. As with business unit driven SaaS adoption, this empowerment has the potential to grow the disruption gap unless proper visibility into application usage is established.

The abstraction from detail the cloud provides enables business users to construct data centers, build and maintain new services by chaining functionality, and apply on-the-fly adaptations. The cloud has empowered business users directly from their desktops.

Technology is no longer confined to the IT department; tech is embedded into the fabric of our lives. The modern smartphone has more computing power than the mainframes of the 1970s. According to Ericsson, global mobile subscriptions reached 7.5 billion in 2016, up from 5.3 billion in 2010[iii]. In the same period, the number of applications available in Google Play has risen from 30,000 to 2.4 million (September 2016)[iv]. The modern workforce is tech savvy, capable of managing their own IT resources, and accustomed to instant resolution of need – if functionality isn’t available from one source, then download it from another.

The reliance on digital technology in our private lives and ever-rising performance and flexibility of personal computing technology outstripping standard corporate approved devices and software, are two of the factors contributing to the bring-your-own-device (BYOD) movement. Today we are moving into a new generation of BYOD. Any perceived slowness in service delivery causes users to circumvent the approved IT practices that safeguard enterprises from license compliance, overspend, and security risks.

CONCLUSION

Cloud adoption, consumerization of IT, and shifting user behavior are profoundly disruptive forces, affecting both business and IT operations. These forces are growing the disruption gap, decreasing IT department visibility into application usage and spend and increasing risk.

By 2020, Gartner predicts that large enterprises with a strong digital business focus or aspiration will see business unit IT increase to 50% of enterprise IT spending.[v]

The trend lines are clear. Spend is shifting from IT to the business. Embracing this shift though astute distribution of control to maintain visibility is a sure-fire way to maximize the benefit of cloud technologies, automation, and consolidation; avoiding costly software audits, virtualization sprawl, and uncontrolled device usage. Forward thinking IT leaders will use 2017 to embrace the trends affecting software spend and transform their role from control to enablement.

My goal for 2017, is to ensure that your software spend is optimized. Snow will host and attend Software Asset Management events throughout 2017, if you too want to ensure that your software is working for you, check if Snow is holding an event in your region.

[i] http://news.adobe.com/files/press_release/additional/AdobeQ416Earnings.pdf

[ii] http://www.salesforce.com/company/news-press/press-releases/2016/11/161117.jsp

[iii] https://www.ericsson.com/TET/trafficView/loadBasicEditor.ericsson

[iv] https://www.statista.com/statistics/266210/number-of-available-applications-in-the-google-play-store/

[v] Gartner, April 2016, Metrics and Planning Assumptions Required to Drive Business Unit IT Strategies